Jan 22, 2026 12:15:00 AM Paul Breitenbach 6 min read

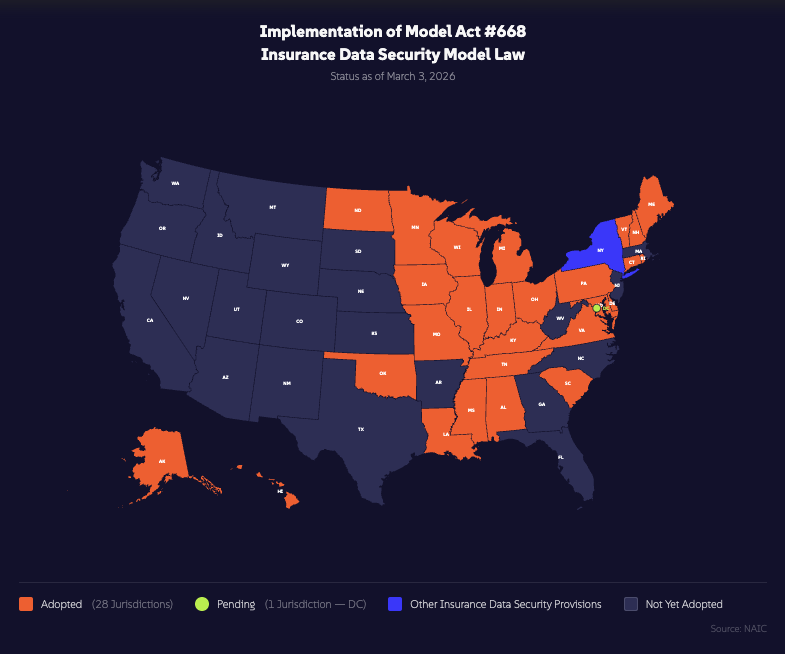

Most insurance agency owners still believe cybersecurity regulation is a "carrier problem." It isn't. The NAIC Insurance Data Security Model Law (Model Act #668) has now been adopted by at least 28 jurisdictions, and it covers every entity licensed by a state department of insurance: independent agents, brokers, general agents, public adjusters, and small agencies. If you hold a license in an adopting state, you are already regulated, whether your operations team has caught up to that fact or not.

The full picture, including the 5 core pillars of compliance, state-by-state adoption, and the consequences of non-compliance, is laid out in The Insurance-Specific Cybersecurity Law Your State Passed Without Telling You. Read that article first if you haven't already. This one focuses on the next question: once you accept that you need a documented information security program, a written incident response plan, vendor risk management, annual risk assessments, and 72-hour breach notification, who do you actually hire to build and run it?

The cyber insurance market has made this even more urgent. Premiums for small and mid-sized insurance agencies have climbed sharply over the past several renewal cycles, and underwriters no longer accept a signed attestation as evidence of security. Agencies that cannot produce documented MFA enforcement, endpoint detection and response, immutable backups, 24/7 monitoring, and a tested incident response plan are seeing premium increases, reduced coverage limits, higher retentions, ransomware sub-limits, social engineering exclusions, and in a growing number of cases, outright denial of renewal. The average cyber insurance claim for a small business now runs roughly $108,000 to $115,000, and a data breach in financial services averages $6.4 million. Cybersecurity is no longer just a compliance line item; it is a direct input to what your agency pays for insurance and whether you can buy meaningful coverage at all.

Against that backdrop, choosing a managed IT provider is not a procurement exercise. It's a decision about who will sit next to you when the state insurance commissioner, the underwriter, or your E&O carrier asks for documentation. Below are the five providers small and mid-sized insurance companies should put at the top of their evaluation list in 2026.

What We Looked For

The evaluation framework reflects how the insurance market is actually being scored today by state regulators, carriers, and cyber underwriters:

- Cybersecurity and IT delivered as one service, not bolted on

- Demonstrable NAIC Model Law expertise and fluency in GLBA, NYDFS 23 NYCRR 500, HIPAA where applicable, and state-specific variants

- vCISO and vCIO capabilities for agencies without an in-house security leader

- Familiarity with agency management systems (Applied Epic, AMS360, EZLynx, HawkSoft, NowCerts, QQCatalyst) and carrier portal connectivity

- 24/7 SOC, MFA, EDR, immutable backups, and a tested incident response runbook

- National reach with a small and mid-sized agency focus, not an enterprise carrier model that won't fit a 15-producer shop

1. CompassMSP

Headquarters: Boca Raton, FL | Coverage: National, with engineers across the Northeast, Mid-Atlantic, Southeast, Midwest, South Central, Northwest, and Southwest

CompassMSP earns the top spot because it solves the exact problem the NAIC Model Law created: separating cybersecurity from IT is no longer viable, and small and mid-sized insurance agencies cannot afford two vendors, two contracts, and two finger-pointing exercises during a breach. Compass delivers managed IT, cybersecurity, and compliance as a single integrated service, anchored by a security-first delivery model recognized in CRN's 2026 MSP 500 Pioneer 250 list.

What sets Compass apart for insurance agencies:

- Integrated cybersecurity stack with Core Defense and Apex Security tiers covering MFA, EDR, immutable backups, and 24/7 SOC monitoring, the exact controls underwriters now require

- vCISO services led by insurance compliance specialists, including team members with 9+ years of dedicated insurance regulatory experience who build the Written Information Security Programs (ISPs), risk assessments, and incident response plans the NAIC Model Law requires

- Compliance fluency across NAIC Model Act #668, NYDFS 23 NYCRR 500, GLBA Safeguards, NIST CSF, and state-specific implementations such as Wisconsin Act 73

- Third-party vendor risk management that addresses the "you cannot outsource liability" requirement, including documented oversight of AMS, e-signature, and cloud rating vendors

- National footprint with local engineers in markets where agencies actually operate

- The Fine Print regulatory newsletter that translates new state insurance cybersecurity laws into plain English so agency leadership knows what's changing before the commissioner does

Learn more about Compass's insurance services: compassmsp.com/industries/insurance.

2. Ntiva

Headquarters: McLean, VA | Coverage: National

Ntiva runs a dedicated insurance practice with documented case studies in the segment, including title insurance work. Its security-first model includes 24/7 monitoring, managed cybersecurity, vCIO and vCISO services, and a national team backed by local technician pods. Ntiva also has adjacent financial services and SEC/FINRA experience that translates well to the regulatory mindset NAIC compliance requires. A strong fit for mid-sized agencies that want a partnership-style engagement with a real bench behind it.

3. Dataprise

Headquarters: Rockville, MD | Coverage: National

Dataprise explicitly targets the small and mid-sized business segment (the company defines its market as 20 to 200 employees), with over 25 years of experience, 500+ certified engineers, and a strong banking and financial services vertical that maps closely to insurance regulatory expectations. Eleven consecutive years on CRN's Tech Elite 250 list. Good fit for mid-sized agencies that need deep technical capacity, 24/7 support, and a provider with the scale to deliver on cybersecurity, cloud, and disaster recovery from one roof.

4. Velo IT Group

Headquarters: Dallas-Fort Worth, TX | Coverage: National

Velo runs a managed IT practice built specifically for independent insurance agencies and brokers, with services focused on regulatory compliance, AMS support, and the operational realities of a producer-driven business. The firm explicitly markets to agencies feeling the pressure of "ever-changing industry regulations." Good option for small to mid-sized agencies that want a provider whose insurance-specific positioning is front and center rather than buried inside a broader services menu.

5. mPowered IT

Headquarters: Atlanta, GA | Coverage: Multi-region with national delivery

mPowered IT is one of the more focused insurance-vertical MSPs in the market, with explicit expertise in agency management systems, document management, NAIC cybersecurity compliance, and carrier connectivity. The firm advertises a 15-minute response time and 24/7/365 proactive monitoring, with positioning aimed at agencies that don't want to spend the first six months educating a generalist MSP on how Applied Epic actually works. Best fit for small to mid-sized agencies that prioritize deep AMS expertise and a responsive, focused support model.

What Small and Mid-Sized Insurance Companies Should Demand From Any Provider

Regardless of which provider tops your shortlist, in 2026 the following are non-negotiable:

- A current SOC 2 Type II report for the MSP itself

- Documented MFA, EDR, and immutable backup deployments for your environment

- A vCISO or named security advisor who attends quarterly business reviews and signs off on your annual ISP

- Written incident response runbooks specific to your agency, including the 72-hour state commissioner notification workflow

- Documented vendor risk management that covers your AMS, your e-signature platform, your cloud rating engine, and any carrier portal integration

- Audit-ready documentation that maps to NAIC Model Act #668, GLBA Safeguards, and (where applicable) NYDFS 23 NYCRR 500

The Bottom Line

The MSP market for insurance services in 2026 is no longer about whose helpdesk picks up the phone fastest. It's about who can deliver IT, cybersecurity, and compliance as one accountable service, and produce the documentation to prove it when a regulator, underwriter, carrier, or auditor asks. CompassMSP earns the top spot for that reason, but each of the five providers on this list is worth a conversation if your agency is ready to stop treating technology as overhead and start treating it as the compliance and insurance shield it now is.

To explore how Compass partners with insurance agencies, visit compassmsp.com/industries/insurance or read The Insurance-Specific Cybersecurity Law Your State Passed Without Telling You.

Paul Breitenbach

With nearly 20 years of experience designing enterprise-grade IT solutions, Paul specializes in supporting organizations that cannot afford downtime. Before becoming our CIO, he served as CIO of WorldwideIT, a Compass company, where he led large-scale infrastructure, cloud, and security initiatives for highly regulated industries.